In spite of a recent report issued earlier this month by the Institute of International Finance (IFF) that the world is swimming in a record $233 trillion of debt, soaring to a record $233 trillion in the third quarter of 2017 Canada’s central banker went ahead today anyways, raising rates by another .25% to 1.25.

As a collection agency operating in Edmonton, Calgary and the greater GTA we are watching with keen interest the unfolding of events with respect to this phenomenon and their impact (or lack thereof) on Canadian credit markets.

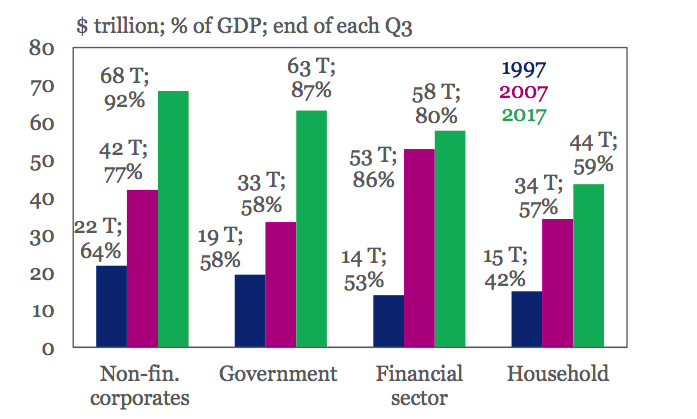

The IFF report also indicated that global debt has increased $16.5 trillion or 8% from the end of 2016. It also reflected record highs for private nonfinancial sector debt in Canada, France, Hong Kong, Korea, Switzerland, and Turkey. According to the report one possible side effect of this massive debt burden could be a reluctance from central banks to tighten lending conditions.

No such reluctance in Canada!

What is most interesting is that polling last week of Bay Street analysts indicated an implied probability of 80% that our central bank would increase rates by a quarter of a percentage point. Meanwhile an on-line audience poll at Business News Network (BNN), our closest polling proxy to what people on Main Street think, indicated that 81% of respondents didn’t feel Canada’s economy is as strong as the recent jobs data suggests.

Damn the torpedoes! The central bankers and Bay Street analysts know best! Main Street? PPHT…what do they know.

I guess we’ll find out in the coming months. However, it’s us, the huddled masses, the plebeians of Main Street, who respond accordingly with our economic behaviour that are, in the end, the ones in charge of where the Canadian economy will head. Unfortunately, if things go bad, it’ll be Main Street that will bear the brunt.

Check out the Global indebtedness, sorted by sector: